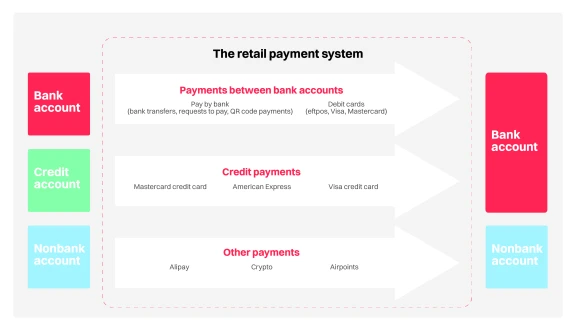

Our payment system

New Zealanders make and receive payments in many ways. These payment options work in different ways and involve different participants in the system.

We’ve broken down some common ways to pay and outlined some of the key concepts and participants in our payment system.

Common ways to pay

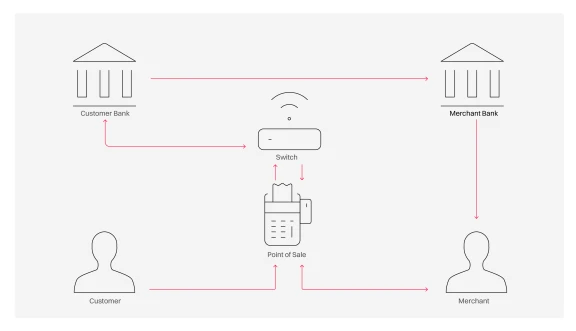

In store EFTPOS and contacted debit payments

These are transactions where you pay in store by swiping or inserting a physical card and selecting debit or savings and entering your PIN.

The process

-

Customer uses their EFTPOS or debit card at a payment terminal to initiate the payment process.

-

The business’ payment terminal connects with the customer’s bank electronically to request the payment amount from the customer’s account associated with the card (often described as cheque or savings).

-

The customer’s bank either accepts or declines the payment request.

-

If the payment is accepted the amount is transferred to the businesses account.

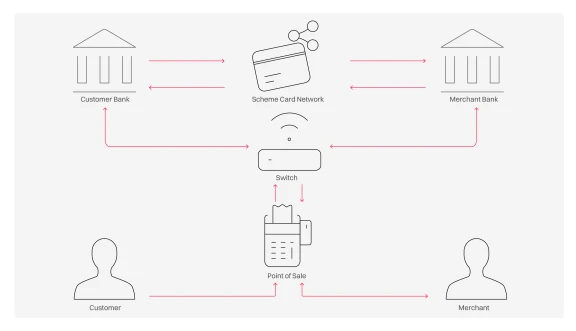

In store contactless and credit card and contactless payments

These are transactions where you pay with a debit or credit card by or tapping your physical card, mobile phone (via a digital wallet) or wearable (watch), or by swiping or inserting a credit card.

The process

-

Customer uses their credit card at the payment terminal to initiate the payment process.

-

The business’ payment terminal electronically connects with the business’ bank, who then send the payment request to the card scheme (eg, Mastercard, Visa) who pass that request on to the customer’s bank for authorisation.

-

If the customer’s bank authorises the payment, the transaction is accepted and is passed back to the business’ bank and then shows as accepted to the business at point of sale.

-

The customer’s bank takes the money from the customer’s account, and the businesses’ account is credited by their bank.

Online card payments

These are transactions where you pay using a credit or debit card online or in an app by entering your card details.

The process

Online card payments are processed in similar ways to in person card transactions.

There are two differences:

- the point of sale is replaced with the website or app, and

- the switch is replaced with a gateway and payment processor.

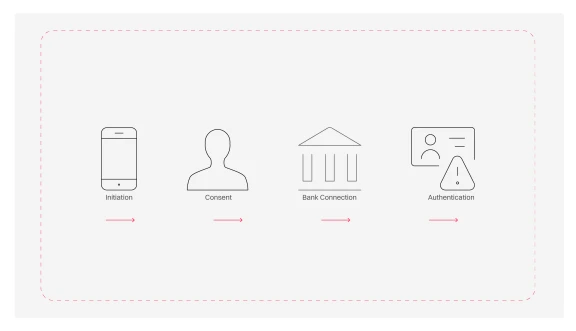

Payments enabled by open banking

Open banking is wider than just payments, but we have a specific interest in the payments aspect. Payments using open banking happen where a customer consents to an open banking provider (eg, fintech) facilitating a payment from that customer’s bank account. The open banking provider must be accredited as meeting specific legal standards to facilitate payments or share information and have secure connections to the banks to send these messages (an API connection).

The process

-

Customers use their phone to scan (in person), or request to make 'open banking' payment in-app or at online checkout.

-

The accredited open banking provider communicates the details of the proposed transaction to the customer's bank.

-

The customer approves the transaction in their banking app or internet banking (in some cases a customer may choose to pre-authorise these transactions, similar to a direct debit or credit).

-

The money is taken out of the customer’s account and the amount is credited to the business’ account.

Common payment terms explained

- Issuer (customer’s bank) – This is the bank or other financial institution that gives a customer their debit or credit card. When a customer pays, the issuer checks and approves the payment and sends the money from their account.

- Acquirer (the business’s bank or payment provider) – This is the bank or payment provider that helps a business accept card payments. The acquirer receives the money from the issuer and deposits it into the business’s account.

- Payment processor – The processor securely moves payment information between the customer’s bank and the business’s bank. Processors may also provide services like fraud checks or support for different currencies.

- Switch – A switch routes the payment information to the right place.

- For EFTPOS or contacted debit cards, it sends the details to the issuer.

- For credit or contactless cards, it sends them to the acquirer.

In New Zealand, Verifone and Worldline operate the main switches.

- Terminal provider – These companies supply the payment terminals used in stores. Newer terminals also support QR codes for open banking payments and often integrate with inventory or accounting systems.

- Payment Gateway – A gateway is used in online payments and payments at self-service terminals. It collects the customer’s payment details on a website or app and sends them securely to the processor or acquirer.

- Open banking payment providers – These companies let customers make payments directly from their bank account using a secure connection. This can be:

- person‑to‑person (eg, buying something second‑hand)

- customer‑to‑business (online or via QR codes)

- business‑to‑business.

They must be accredited, and accreditation is managed by the Ministry of Business, Innovation and Employment.

Payments Monitoring Snapshots

We’re sharing simple, evidence-based insights into how competition is evolving in New Zealand’s payments system.

Our first edition highlights the growing use of Mastercard and Visa card payments and what this means for the cost of accepting payments for New Zealand businesses.

Our insights draw on information from businesses, consumers and payment providers, including emerging payment options such as pay by bank, to understand what is shaping outcomes in practice.

Please pass on any feedback on the insights in this snapshot, including any evidence that could improve our understanding of how the system is developing. Feedback can be provided to: PaymentsTeam@comcom.govt.nz

Research

From time to time, we expect to carry out surveys to better understand how the retail payment system is performing to inform our work.

In 2022, we worked with Kantar Public to survey New Zealand businesses to better understand their experiences and perspectives on the retail payment system.