Merchant Service Fees

Businesses are charged a Merchant Service Fee to accept contactless and credit card payments.

Merchant Service Fees are paid to a business’ payment service provider, which may be a bank, specialist payment firm, or point of sale service.

There are two common pricing plans for these fees.

- Blended (Fixed) pricing

The business is charged based on a simple fee structure that often has a single or few rates. Blended pricing offers certainty of costs, which is useful for some businesses. - Interchange Plus (Unblended) pricing

The business is charged the interchange fee plus the additional costs to process the fee and a margin for the payment service provider. The pricing for each transaction type differs depending on the card the customer uses (eg, debit, credit) and how they choose to pay (eg, in-person, online). This pricing plan is often cheaper for most businesses, but is less certain to predict.

What makes up a Merchant Service Fee?

A Merchant Service Fee is usually made up of:

-

Interchange fee

-

Scheme fee

-

Transaction fee

-

Acquirer margin

We’ve set limits on how much can be charged through Interchange fees, which is the largest component of Merchant Service Fees.

Read more about Interchange Fee regulation.

Comparing Merchant Service Fees

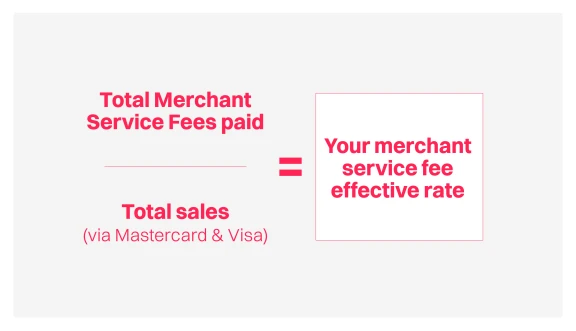

We want businesses to understand their Merchant Service Fees so they can shop around for the best deal for them.

Working out your effective Merchant Service Fee rate is an important first step to understand how different providers compare. It’s important to remember that lower rates are only one aspect to compare, as some providers bundle in other services and support that are helpful for smaller businesses.

Working out your Merchant Service Fee

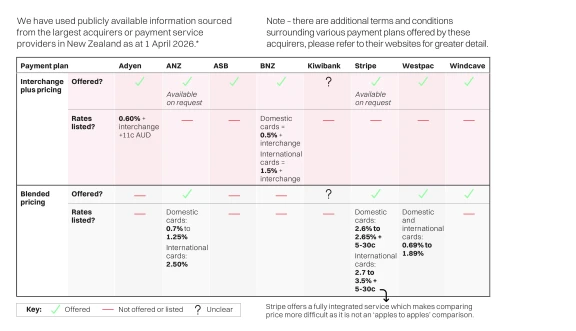

How do different providers compare?